Internal Revenue Items – CBMA Declarations

If your item is subject to internal revenue tax, you can enter the required information at the Article level under the Additional Declarations tab.

Effective January 1, 2023, importers seeking to take advantage of assigned tax benefits must pay the full tax rate to U.S. Customs and Border Protection (CBP) at the time of entry. A refund claim must then be submitted to the Alcohol and Tobacco Tax and Trade Bureau (TTB).

CBMA information for a future refund must be submitted at the time of entry, as outlined below.

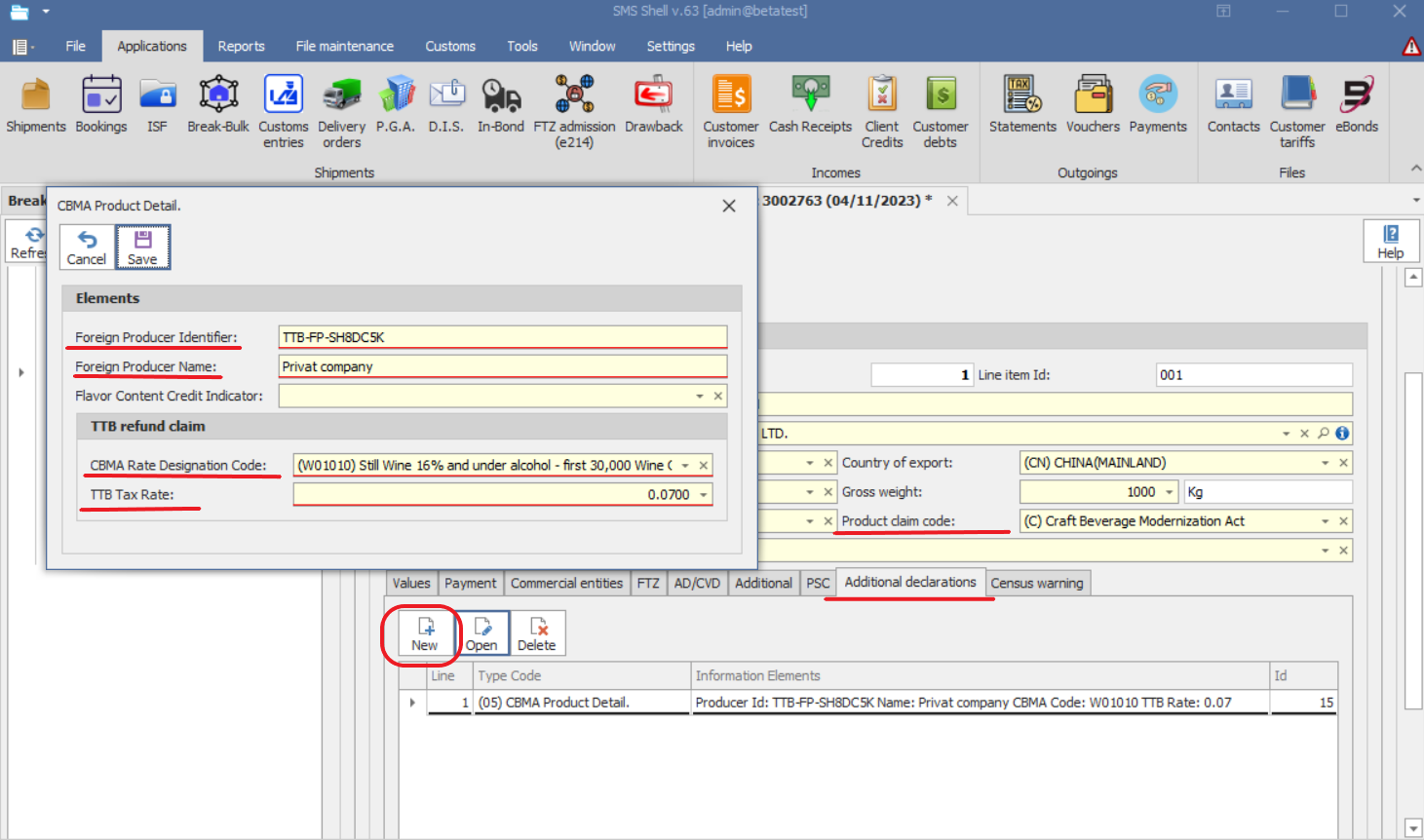

Required CBMA Entry Information

1.Product Claim Code

oEnter Product Claim Code “C”.

2.CBMA Product Detail Declaration (Code 05)

Add the declaration for (05) CBMA Product Detail, including the following fields:

oForeign Producer Identifier

The identifying code of the foreign producer or assigning entity.

oForeign Producer Name

The full name of the foreign producer or assigning entity.

oFlavor Content Credit Indicator

For spirits only: indicates that the importer used an eligible flavor content credit rate when determining the effective tax rate.

oCBMA Rate Designation Code

oTTB Tax Rate

To view applicable CBMA tax rates, refer to the following resource:

Please follow this link for more information:

Tax Benefits under the Craft Beverage Modernization Act (CBMA)